Spear’s Property Advisers Index 2021 – Full House for Forsters

25 March 2021

News

Listing only the key advisors in the UHNW real estate sector, the Spear’s Property Advisers Index 2021 features the industry leaders advising high net worth individuals on prime and super-prime residential property.

We are delighted to announce that all of our Partners in the Residential Property team have been recognised as ‘the best property lawyers‘ in the index this year, with the following rankings:

In addition to our Partners, Adam Whitfield Jones, Senior Associate in Residential Property, has been recognised as a Rising Star.

With a total of five lawyers, Forsters is the firm with the greatest number of advisers ranked in the index. The recognition is a testament to the unparalleled reputation and strength of the team and their expertise.

As the largest specialist team dedicated to Residential Property in London, our lawyers can provide an unrivalled level of service to clients. To learn more about our lawyers, and the services they can provide for you, please visit our luxury property hub.

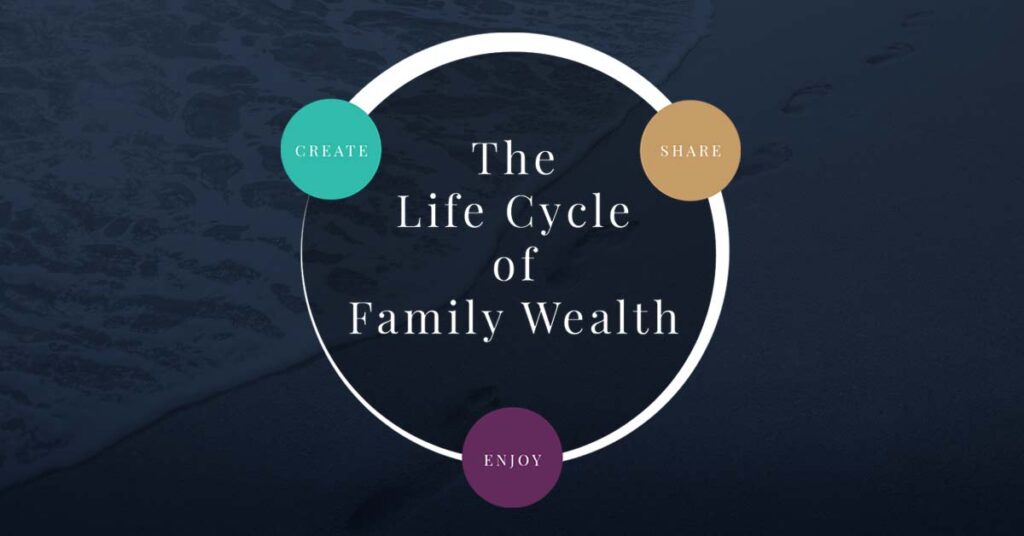

From growing a business to starting a family or handing over control of that business to the next generation, every individual has their own goals to aspire to. These goals will be shaped around key life milestones and will change depending on what stage in life a person has reached. As these milestones approach, this will often be a time to reflect, resulting in a change in priorities and a different focus for both their wealth and family.

Our Private Wealth lawyers advise our clients throughout this family life cycle, providing the legal advice required for specific transactions such as purchasing a home or selling a business, whilst also advising on the long-term opportunities for succession and estate planning.

In our experience there are three key priorities for individuals and their families with regards to their wealth – to create, share and enjoy it. Forsters Private Wealth are here to support families achieve their ambitions; our overarching purpose is to assist clients to grow, preserve and protect their wealth so that they can focus on what matters to them, no matter what stage in life they have reached.

Read on to find out what issues individuals and their families need to consider at key milestones in life and how we can support and advise our clients to achieve their ambitions.

The post-COVID bounce back in M&A deals has led a lot of entrepreneurs to consider selling their businesses. Business owners are aware that today’s extremely healthy M&A market will not continue indefinitely and that the window of opportunity will soon begin to close.

Governments recognise that encouraging people to start businesses and employ others is important for the economy, and that any charge to tax on disposal should be mitigated to recognise the years of work involved in building a business, and the financial risk that people take in doing so.

This was the principle behind Business Asset Disposal relief (BADR), formerly Entrepreneurs’ relief, when it was introduced in 2008 to replace the earlier Business Asset Taper Relief. Over the intervening years, its conditions have been toughened and the lifetime limit of capital gains able to qualify for the relief has been reduced from £10 million to £1 million with effect from March 2020.

Nevertheless, to the extent it continues to be available, BADR is a valuable tool for business owners to minimise the tax payable on a disposal of a business or an interest in it, reducing the rate of CGT on qualifying capital gains to just 10%.

However, it should be noted that, if the individual disposes of other capital assets in the same tax year, then the gains benefiting from BADR use up any remaining part of the disposer’s basic rate band, forcing the other non-property gains to be taxed at 20%.

Disposal of shares in a trading company

The requirements for claiming BADR for a sale of shares in a trading company are that there is a disposal by an individual (or in some cases trustees) of:

shares in a trading company where the seller was an employee or officer of the company, and

in which they had owned at least 5% of the ordinary share capital, and

with the ability to exercise at least 5% of the voting rights,

each for at least two years ending on the date of disposal;

The seller must also meet one or both of the following two tests throughout the relevant two-year holding period:

have at least a 5% interest in the company’s distributable profits and be entitled to at least 5% of the assets available to equity holders on a winding up, and/or

be entitled to 5% of proceeds in the event of a disposal of the whole of the company’s ordinary share capital.

There may be some relief if the 5% shareholding is diluted by the further issue of shares – assuming that issue was for commercial purposes.

For the proceeds test there are three assumptions – firstly, that the whole of the ordinary share capital is disposed at its market value on the final day of the period, secondly, that the seller’s share of the proceeds is the amount that the seller would reasonably expect to be beneficially entitled to at that time and, thirdly, the effect of avoidance arrangements is disregarded.

There is also a provision designed to help business owners who, by an issue of new shares, would cease to be eligible for the relief. This allows the owner to determine the amount of gain they had made on the period they were entitled to the relief by a deemed disposal and reacquisition. The owner can then defer that gain until they actually dispose of the shares, and thereby avoid incurring a “dry” tax charge.

What happens if the company ceases to be a trading company?

If a company ceases to be a trading company, BADR may still be available if the shares are sold within three years of the date on which the company ceased to trade.

Extra care needs to be taken if the disposal is not a third-party sale but the receipt of a capital distribution following the winding up of the company.

Other disposals qualifying for BADR

BADR may also be claimed (subject to the £1 million lifetime limit) for any of the following disposals, provided, again, that they are made by an individual (or trustees, in certain circumstances):

The transfer of all or part of a business the seller had owned as a sole trader or business partner for at least two years, ending on the date of disposal;

A disposal of assets used for the purposes of a business at the time when the business ceased; and

A disposal of personally owned assets (assets the seller owns but that are used by the business) alongside a disposal of at least 5% of the seller’s interest in the business and other related conditions.

If I do not qualify for BADR, are there any other reliefs?

Where BADR is not available for a sale of shares, it may be worth considering Investors’ relief, a relatively new and underused relief that was introduced in 2016. This relief reduces the rate of tax to 10% on lifetime gains of up to £10 million.

It is available on a disposal of ordinary shares in unlisted trading companies by individuals other than officers and employees, or trustees in certain circumstances, and is subject to a three-year ownership period.

The shares must have been issued on or after 17 March 2016. However, as with BADR, there are detailed conditions that must be satisfied to qualify for the relief.

Where appropriate, it may be worthwhile selling a substantial shareholding to an employee ownership trust (EOT). Such a disposal would not be subject to any capital gains tax but requires a range of other issues to be considered. These will be discussed in a different article.

And finally…

If you have any questions regarding BADR or Investors’ relief, or in connection with a disposal of shares or a business more generally, please get in touch with a member of our Private Wealth or Corporate Tax teams.

Elizabeth Small is a Partner and Oliver Claridge is an Associate in the Corporate team. Nicole Aubin-Parvu is a Knowledge Development Lawyer in the Private Client team.

From growing a business to starting a family or handing over control of that business to the next generation, every individual has their own goals to aspire to. Our Private Wealth lawyers advise our clients throughout this family life cycle, providing the legal advice required for specific transactions such as purchasing a home or selling a business, whilst also advising on the long-term opportunities for succession and estate planning.

Making and updating a Will: a crucial estate planning tool

23 March 2021

News

Making a Will is a vital part of any estate planning exercise. Sharing wealth with family and other loved ones in the most tax efficient way possible, is a priority for most people. Their aim is to provide for partners and ensure that children are supported financially to achieve their goals, whether those include buying a property, or starting a family or business.

Given this strong desire to share their wealth, it is concerning that nearly two thirds of adults in the UK do not have a valid Will in place. Statistically, a high proportion of these will continue to have no Will at their death. This means that their estates will be distributed to whichever family member stands in line to benefit under the intestacy rules, and with no choice of who acts as executor.

What happens if you don’t have a Will?

As an example, if someone dies intestate (without a will) leaving a spouse and children, the spouse will have the right to:

Administer the estate.

Inherit all the personal belongings.

Inherit a legacy of £270,000 and one half of the remaining estate.

The balance of the estate will pass to the children in equal shares. This will rarely be the result that the deceased would have chosen.

In fact, dying intestate can be the catalyst for serious friction within a family that, in the worst cases, may end in litigation. Every family is different, with unique dynamics between family members that a Will can help to accommodate. A testator may be part of a cohabitating couple, or in a second marriage or civil partnership. There may be children or step-children (or both) with whom they may or may not get on. They may have adopted children or, increasingly, their children may have been born by way of surrogacy, which raises its own inheritance issues. Adult children or step-children, in turn, may be in difficult relationships with spouses, civil partners, boyfriends or girlfriends.

It is also worth noting that intestacy can have unfortunate inheritance tax consequences which it may be possible to mitigate with a Will.

Why make a Will?

Such complex relationships provide strong reasons for individuals to ensure they have a Will in place. However, even those with more straightforward family arrangements should make a Will to ensure that their spouse, civil partner or other partner, children and members of their wider family, receive the gifts and shares of their estate that they wish to leave, and that the people they wish to administer their estate are appointed to do so.

Many people also choose to appoint guardians for their children in their Wills. While this can be a good approach, choice of guardians can sometimes be one of the most difficult decisions for a couple to make. As such, it is important not to hold up signing a Will because this issue remains outstanding. Once guardians are chosen, a separate deed can be drawn up or a couple’s Wills can be updated, whether by making a new Will, or using a separate document, known as a Codicil, which is read as if it was part of the Will itself.

Life events and other reasons for updating a Will

There are many reasons for updating a Will. A testator’s choice of executors or guardians may be out of date. They may have changed their mind about legacies; who should benefit or how much they should receive.

There may be a statutory reason, for example, where trusts have been set up in a Will that now need to last into the grandchildren’s generation and beyond. Before April 2010, the fixed period a trust could last was limited to 80 years. This has been extended to 125 years, and Wills that pre-date this change should be changed to take advantage of the longer period.

Significant life events may affect the validity of an existing Will, or the nature of the legacies within it.

Marriage or civil partnership

Unless a Will is made expressly in contemplation of marriage or civil partnership, it will be revoked automatically on either of these events taking place. As such, couples getting married or entering into a civil partnership should ensure that they make new Wills or Codicils, either in advance, clearly stating their intention to marry or become civil partners, or as soon as possible following the ceremony.

The arrival of children

The arrival of children is an exciting, but incredibly busy time. However, it is obviously important to ensure that children are properly provided for in the event of a parent’s untimely death. Many Wills will already include gifts in favour of future children, but even if this is the case, it is important for parents to re-visit their Wills to ensure that such gifts continue to reflect their intentions.

Divorce, second marriages or civil partnerships and second families

Divorce or the dissolution of a civil partnership does not invalidate a Will, but instead the Will is read as if the former spouse or civil partner had pre-deceased the testator, and his or her estate passes accordingly. While this may be what the testator would want, that may not always be the case. In any event, it is a good idea to revisit the terms of a Will following a divorce.

Once again, any subsequent marriage or civil partnership will invalidate a pre-existing Will unless made in contemplation of this event, so individuals should review their Wills before, or as soon as possible after, getting married. This is particularly important, because consideration will be needed to ensure that legacies take account of any children (or grandchildren) of the previous marriage, as well as the needs of a new family.

Updates to take account of legal changes

Transferable nil rate band: Changes to the law made in October 2007 mean that it is no longer necessary to make specific provision in a Will for the use of the nil rate band (the value of a Testator’s estate which can pass tax-free to any beneficiary, currently £325,000)). This band is now transferable to the estate of the surviving spouse or civil partner in the event that it is not fully utilised on the death of the first to die. When updating their Will, testators may choose to remove a nil rate band trust or other gift where one is included, in favour of a different type of legacy.

Residential nil rate band: Another, more recent, nil rate band-related change applies to estates that include a residential property that has been the main residence of the deceased. If this passes to a child or other direct descendant of the deceased, an additional £175,000 “residential nil rate band” may be available (£350,000 if the transferable nil rate band from the other spouse is available). There is a tapering of the relief for estates with a value over £2 million, so this nil rate band will not be available in all circumstances.

In most Wills, such a property would be left to a spouse and then to children, or to children directly. However, where this is not the case, testators may wish to revisit their Wills to take advantage of the residential nil rate band where it is available.

Trusts – discretionary or life interest: Historically, Wills often included a life interest trust, initially naming the surviving spouse as the life tenant (who would be entitled to the income of the trust during their lifetime) and then for children and grand-children.

More recently, following changes made in 2006, such trusts have fewer tax advantages than in the past over discretionary trusts, at least once the surviving spouse or civil partner has died. Consequently, many more Wills nowadays for testators with a significant asset base, are set up as a flexible discretionary trust, rather than a life interest trust. The discretionary trust will name the close family members who are to benefit and will often include a power given to the trustees to add further beneficiaries at a later date.

The precise wishes of the testator are set out in an accompanying (but non-binding) side letter just as they can be with a life interest trust. The letter can say whatever the testator wishes in his or her own style. It has no specific legal format and can be updated by the testator at any time to take account of changes in circumstances and without going through the formalities of preparing a new Will.

Such a format provides significant flexibility. Testators can provide guidance to the trustees as to how their property should be distributed, or how their business should be run, and by whom. At the same time, the trustees are not bound by these wishes, as they would be by clauses in a Will, and can adapt them to take account of different scenarios as they arise. For example, if a potential beneficiary is in a difficult relationship, or is likely to be divorced, the trustees will be able to monitor how and whether he or she receives income or capital, and consider how best to avoid an inheritance falling within a financial settlement.

Where a discretionary Will is not the solution

A discretionary Will may not suit every situation. A couple may prefer more clarity, perhaps because theirs is a second marriage for one or both of them, or they are troubled by the non-binding nature of the side letter. However, where a Will contains a trust, whether it is discretionary or includes a life interest, testators should consider carefully the level of freedom they want to give their executors, trustees and guardians (where relevant) as the ultimate decision-makers.

International considerations

Additional considerations apply to individuals with international connections. Anyone who is resident outside England and Wales, but who owns property in this country, or who is resident here with property abroad, should take advice on how best to ensure a smooth succession to their assets wherever they are located.

The domicile of the individual concerned may also be relevant. Under the general law of England and Wales, the place where an adult is domiciled may vary during their lifetime. It will depend on whether they retain their domicile of origin (generally where their father was domiciled at the time of their birth) or have acquired a different domicile of choice (the place where they intend to live permanently or indefinitely).

This may be relevant in the context of succession to their estate because under the law of England and Wales, the law of the place where property is situated governs the distribution of immovable property (e.g. their residence or commercial property). On the other hand, an individual’s movable property (e.g. cash, bank accounts, shares, works of art etc) passes according to the law of the individual’s domicile at death.

For this or other reasons, in some cases, it may be advisable for an individual to have more than one Will, each dealing with property in different jurisdictions. In addition to the legal issues, practically this may help to ensure that such property can be dealt with and distributed as quickly and efficiently as possible following their death.

If a testator has more than one Will, care must be taken to ensure that those made in different jurisdictions do not contradict, or even revoke, each other. It is also vital to ensure that the intended gifts can be made under the law of the relevant jurisdiction. Legal advice in each jurisdiction in which property is held should always be taken, whether a local Will is being made, or all property is to pass under a single Will.

Next steps

An up-to-date Will is essential to ensure that wealth is passed on in accordance with the testator’s wishes. Therefore, if there has been a change in personal or family circumstances, it is a good idea to review an existing Will or to arrange to make one (if there is not one already).

To find out more about Wills and consider the best way to proceed, please do get in touch with a member of our Private Wealth team.

Anthony Thompson is a Partner in the Private Client team.

A PDF copy of the article above is also available to download here.

Why is a family investment company a good way to pass on wealth?

22 March 2021

News

In the past, if people wanted to pass wealth to their children (often prompted by the prospect of ultimately paying inheritance tax if they did not) they would use trusts, because then they could keep the assets under their control.

Over a decade ago the government made that no longer viable for most UK based individuals by:

Imposing a charge of 20% when assets (over the first £325,000) are put into a trust.

Making trusts subject to the highest income tax and capital gains tax rates.

For families with assets eligible for relief from inheritance tax – a trading business, a farm, or “risky” investments like AIM and EIS shares – trusts are still very useful, but not so for those holding traditional investments or cash.

Although this article is written from a UK perspective, family investment companies can be just as useful for international clients; a trust is not always the right vehicle, and not every family feels comfortable involving a professional trust company.

If, for whatever reason, a trust or a simple outright gift to children is not appropriate, what are the alternatives? Some years ago much was made of so-called family limited partnerships, and while they remain the right vehicle for some, they are appropriate only for those with at least £10 million to spare because of the financial regulations to which they are subject. Enter the family investment company.

What is a family investment company?

The parents create the company and fund it with cash. They are the directors and the holders of all the voting shares, and their children are given a non-voting share each. That means that if one of the children needs money, the parents can declare a dividend in his or her favour.

The parents are in complete control of the company, but they have reduced their taxable estates because their shares carry no economic rights, only voting rights. There is a further degree of protection because, while the children hold shares outright, the articles can from the outset prohibit the transfer of shares to anyone who is not a descendant of the parents.

In due course, when (for instance) the children are in secure relationships and sufficiently responsible, the parents can bring them onto the board and give them voting shares.

The parents have, therefore, reduced their taxable estates by shifting value to the children, but without handing over control.

Tax benefits

In addition, family investment companies are increasingly attractive thanks to their very favourable tax status:

Funding the company carries no tax charge.

When the company buys stocks, it pays 0.5% stamp duty exactly as individuals do.

Currently, the company will pay only 19% on any profit it makes on the sale of underlying investments. Come 2023, that rate will be preserved for companies with profits below £50,000, while larger companies may pay up to 25%.

When determining the company’s taxable profit, the investment manager’s fees are deductible.

Dividends declared on almost any kind of underlying equities are tax-free in the company’s hands.

If the company itself declares a dividend, the tax rate depends on the income of the recipient. In the example above, if the daughter is at university and therefore has no income, dividends of up to £14,500 can be paid to her tax-free (i.e. her dividend allowance of £2,000, plus her personal allowance of £12,500). The next £37,500 will attract only 7.5% tax.

Limitations

All of that makes family investment companies very appealing. To give the full picture, though:

If the family are higher rate taxpayers and receive regular dividends from the company, they will be making little use of the benign tax environment the company offers: to the extent that income from the underlying investments flows immediately through to the family, it will be taxed exactly as if the investments were held directly.

Although the company is not a one-way street, it can be expensive to undo. If the family wanted to get the assets back into their own hands, they would need to redeem their shares or wind up the company. Doing so would give rise to capital gains tax on the amount by which the shares had increased in value.

The example given above is a simple one, suitable for the family in question. No two families are the same, and for another a more complicated entity might be suitable.

How we can help

We have significant experience of creating these types of companies, from those for nuclear families, to those for extended families living in different parts of the world with professional advisers acting as trustee shareholders.

To find out if a family investment company is the right approach for passing on wealth to your family, please do get in touch.

How to protect the “bank of mum and dad” when your child is cohabitating

19 March 2021

News

Q&A: I have recently provided my daughter with funds to buy a flat in her own name and she wants her boyfriend to move in. Could he have a legal or financial claim on the property if they split?

Unmarried, cohabiting couples are the fastest-growing type of family, with an increase of over 25% in a decade.

As house prices continue to rise faster than average incomes, many young people are turning to the “bank of mum and dad” to help with their first property purchase.

Whilst such scenarios are increasingly common, they give rise to a number of legal issues.

Funding a purchase for a family member

It is important to think carefully about the help you are agreeing to provide, and to be clear with your daughter about the terms on which you are providing it.

Will you be lending the funds, or making a gift? There can be tax advantages to making gifts during your lifetime but a gift is irrevocable, and you should only make a gift if you can truly spare the money. You also need to bear in mind that, once you have made a gift, you have very little control over what the recipient does with it.

A loan does not have the same tax advantages of a gift, but it can provider greater flexibility. It is important to be clear about the terms of any loan – what it is to be used for, when it is to be repaid, and whether interest will be charged.

You also need to bear in mind that a court may look behind the loan documents when deciding whether there is a true expectation that a loan will be repaid. There are many cases where courts have decided that a loan between family members is “soft” and that the lender will not in reality insist on repayment.

A properly drafted loan agreement, clearly setting out the terms of the loan, is essential. If the loan is to assist with a property purchase, you should consider registering a charge against the property, in the same way a bank or building society would, so that you are notified if the property is sold or another loan is secured against it.

Finally, you need to think about who you are making the loan or gift to. If your daughter and her boyfriend were purchasing the flat in joint names, for instance, you should be very clear that you are making the loan or gift to your daughter, not to the two of them jointly, and you should insist that is reflected in the ownership of the property.

Cohabitation agreement

Ordinarily, your daughter’s boyfriend cannot acquire an interest in her property simply by living in it. However, in reality, it is all too easy for situations to arise whereby he does acquire an interest.

For instance, if the boyfriend received an inheritance, which he used to fund an extension to the property, he could potentially claim that a “resulting trust” had arisen, whereby he acquired an interest to the value of the contribution he made, and any increase in value attributable to that contribution.

Or consider a situation where your daughter and her boyfriend decide to start a family. The boyfriend is in a less well paid job and offers to give it up and become a stay at home father, but he expresses concern that doing so would leave him economically vulnerable if they split up. To reassure him, your daughter promises that “what is hers is his” and that he will always be entitled to half the sale proceeds if they split up. In such a case, there is a real risk the court would decide that a “proprietary estoppel” had arisen, and that your daughter should be held to her promise, because the boyfriend had relied on it to his detriment.

Both those scenarios, and many others, can be avoided if your daughter enters into a cohabitation agreement with her boyfriend. Such an agreement can record the exact terms on which they own and occupy the property and can deal with issues such as:

If the boyfriend is paying rent or a contribution towards outgoings

Whether they expect he will acquire a right to occupy the property, or an interest in it

Who will pay the bills

What will happen if your daughter asks him to move out

Whether furniture will be jointly owned or earmarked as owned by one or other of them.

Marriage

Finally, if your daughter and her boyfriend decide to marry in the future, then the situation changes dramatically. Spouses can make financial claims against one another on divorce, irrespective of how property is owned, and the divorce court can order transfer or sale of property as it sees fit to ensure the parties needs, and those of any children, are met. Where one party has acquired assets before the marriage, or expects to inherit assets during the marriage, they are strongly advised to insist on a prenuptial agreement.

Simon Blain is a Partner in the Family team and Helen Marsh is a Partner in the Residential Property team.

The Life Cycle of Family Wealth

From growing a business to starting a family or handing over control of that business to the next generation, every individual has their own goals to aspire to. Our Private Wealth lawyers advise our clients throughout this family life cycle, providing the legal advice required for specific transactions such as purchasing a home or selling a business, whilst also advising on the long-term opportunities for succession and estate planning.

As Partner and Head of Family at Forsters, and having worked with hundreds of divorcing couples in the past 20 years, Jo Edwards shares her insight into where many marriages go wrong and tips on how to keep yours happy. This article was originally published in Brides magazine.

As a family lawyer and mediator, I have worked with many individuals and couples who have sadly reached the conclusion that their marriage is at an end. After 20 years, this unique perspective has shown some common themes about marriages which don’t stay the course. Although it is right that statistically divorce rates are on the wane, and that this reduction is heavily concentrated in the first decade of marriage, the facts remain stark (from the most recent data available from the ONS), there were over 100,000 divorces in this country in 2019 with the average marriage lasting for 12 years.

So using my experience, here are my top tips for building solid foundations and keeping your marriage happy rather than another divorce statistic.

Tip One – Discuss your goals and ideals before getting married

I have seen many cases, especially where divorce is happening after only a short marriage, where it is clear that the couple entered the marriage with mismatched goals and ideals. That may be about whether (and if so when) to have children, what would be division of responsibilities if they did (stay-at home parent and breadwinner, two breadwinners with childcare etc), how a child may be educated, where they are to live (including where one harbours hopes of moving abroad), the level of involvement of wider family in married life, political and religious beliefs, etc.

There is no substitute for a full, open dialogue about the small print of your marriage before you get wed. Sometimes it is said that it is far too easy to marry but hard to divorce. Have these discussions early on and if you hit any bumps in the road, think about having a facilitated conversation with a therapist to try to reach compromises.

Tip Two – After you marry, never stop discussing your goals and ideals

Even if a couple enters marriage with aligned aspirations, over time priorities change as people grow older. What may have been important to both of you aged 30 may not be the same ten years later. When couples are in the throes of divorce, it is often sadly apparent with hindsight how and when their priorities began to differ and I often think, if only they’d talked. A common example is that, by agreement, one spouse (usually but not always the wife) will give up work to care for children. Over time she may begin to feel resentment about a good career sacrificed and frustrated about feeling financially dependent upon her husband, exacerbated where there is lack of transparency about the finances. Meanwhile her husband may harbour resentment about the expectations of him on both the work and home fronts. Often these resentments fester to the point of no return, whereas early communication could have led to problem-solving.

Tip Three – Be ready to work at the marriage even harder when you have children

Rightly, the arrival of a baby is a joyful time. However, research has shown that as a mother’s bond with a child grows, her other relationships may deteriorate. Couples’ satisfaction with their marriage declines during the first years of marriage, and researchers have shown that the relationship between spouses suffers once children come along (which also tends to be in the early years of marriage). The rate of decline in relationship satisfaction is nearly twice as steep for couples who have children than those who don’t. However, even as the marital satisfaction of new parents declines, the likelihood of divorcing also declines. At the other end, some marriages improve once children leave home, whilst others flounder then when the couple discovers they have few shared interests and there’s nothing keeping them together. All of this highlights the importance of working together as a married partnership to keep things on track after the inevitable chaos a marriage can be thrown into after the birth of a child.

Tip Four – Remember to make time for just each other

It is apparent (though perhaps unsurprising) that time for romance often goes out the window when a marriage is beyond the honeymoon phase and other life pressures (career, children, having to care for elderly parents etc) compete for a couple’s attention. With lots of the couples I see, it’s apparent that there has been no sudden, life-shattering incident – only about 10% of divorces are based on adultery, for example – but rather that they have gradually drifted apart as their attention has been focused away from the marriage.

Many of the unreasonable behaviour petitions I draft contain points like “he prioritised his career to the exclusion of the family”, “she forgot my birthday/said she was too busy to accompany me to an important work function” and the like. I see the whole range of cases, from marriages which haven’t even made it to the first anniversary to those which have lasted 40 years or more. A fellow divorce lawyer, married for over 50 years, used to tell me that throughout his marriage he has taken flowers home for his wife every Friday night. Such gestures, and keeping plenty of “you time”, are vital.

Tip Five – Learn the art of compromise

When I work as a mediator, helping separating couples to resolve issues around money and children, I often ask them how they sorted out disagreements during the marriage as this signals how I may get them to agreement on divorce. Some couples have clearly had a fiery marriage, rife with conflict, and it can be difficult to get them on the same page. With others, it is clear that one is the peacemaker who will invariably back down when there is disagreement; again, this isn’t the bedrock of a happy marriage. The couples I find it easiest to work with in mediation (and who sometimes end up reconciling) are those where there has been low conflict, who can see (if not always understand) the other’s point of view and are willing to work towards common ground, both making compromises in the process. That is the recipe for a happy marriage.

Tip Six – Be open about your finances

Although, increasingly, the families I work with have two successful breadwinners, and the idea of the “norm” being a husband who works and a wife who stays at home to raise children is dissipating, it is still surprising how many cases I do where one spouse knows little or nothing about the family finances. This can leave (usually) the wife feeling insecure and anxious and sometimes this is the main trigger for divorce; in the absence of clarity, that person wants to “cash in their chips” and get a settlement. Instead it is far better to have compete transparency over finances throughout a marriage including joint bank accounts, any salary being paid into them, property in joint ownership, life insurance and Wills providing for each other on death.

Tip Seven – Commit to working hard at your marriage

Sometimes I see someone who has decided, after months or even years of soul-searching and therapy, that their marriage is over. On other occasions I meet a client who is in the throes of an emotional crisis, having only just discovered that their spouse has been unfaithful or behaved in a particular way that has caused upset. To the spouse in the second camp, I always counsel against making hasty decisions in the midst of the storm; sometimes they just need space to think and couples counselling to work out what caused the other spouse to stray and whether a state of forgiveness and trust can be reached.

Someone in an emotional crisis will often ask me, what’s the usual amount of time to wait before making a decision about the marriage? I always say, every case is different. But one thing is certain – every marriage goes through choppy waters. So don’t be tempted to pull the rip cord at the first sign of disharmony; instead, determine to work even harder at your marriage and take it to the next level of contentment.

From growing a business to starting a family or handing over control of that business to the next generation, every individual has their own goals to aspire to. Our Private Wealth lawyers advise our clients throughout this family life cycle, providing the legal advice required for specific transactions such as purchasing a home or selling a business, whilst also advising on the long-term opportunities for succession and estate planning.

Cladding fund papers over residents’ concerns: Andrew Parker writes for The Times

18 March 2021

Views

Construction Partner, Andrew Parker, has authored an article for The Times entitled Cladding fund papers over residents’ concerns.

In his article, Andrew gives context to the announcement from Robert Jenrick that £3.5 billion is being made available to sort the cladding crisis covering ambiguity over the use of the funds, lack of ease to access them and the ability of the construction industry to respond to the increase in demand for cladding related works.

Andrew raises the crucial points that “it is not at all clear from the announcement whether the extra money promised will reach the people that need it” and details the problems in defining buildings which are in scope for government money. “Even the requirement that qualifying buildings be at least 18 metres high is problematic, thanks to an inconsistency in the building regulations, which in one place require the height of the building to be 18 metres, and in another require the floor of the sixth storey to be at least 18 metres.” Furthermore, when it comes to carrying out the remedial works, Andrew points out that “the insurance market is currently running a mile from fire-related cladding works and many professionals are simply unable to obtain any cover at all â where does that leave prospective applications?”

The full article can be accessed here, behind the paywall.

Special purpose acquisition companies (SPACs) have been around for a while and although they may have “historically been viewed as a bit shady” (Axios correspondent Felix Salmon), 2020 seemed to have been (at least for them) a good year, with SPACs (particularly in the US) being increasingly used as a means for established private companies to access capital markets and go public.

So, what are SPACs?

Simply put a SPAC is a company that is formed to raise investment capital through an initial public offering (IPO) in order for them to acquire an existing operating company. Often referred to as “blank cheque” companies, a SPAC is created to raise funds through an IPO, with the capital then being held in a trust until a predetermined period elapses or the desired acquisition is made. If the acquisition is not made within a certain period (usually two years), the SPAC has to return the funds to the investors.

The re-invention of the SPAC?

Over the past 12 months, SPACs seem to have re-found favour as sponsors have identified them as an option in their investment armoury. According to Dealogic, 256 SPACs were listed last year, compared to just 73 in 2019, while a recent New York Times article has reported that in the US $42.7 billion was raised by SPACs during January and the first half of February 2021 alone, with many sports personalities, celebrities and well-known investors becoming involved.

Despite the hype surrounding them, SPACs are relatively straightforward structures to create and to understand, with the sponsor merely needing to create a company, undertake the requisite filings that go with the incorporation of a public company and then find investors to buy units in the company. Investors generally acquire a unit that represents one share in the company, along with a warrant that gives them the ability to buy more shares in the future. The attraction for the sponsor is that they usually retain a 20% stake in the SPAC, which can be considered “founder shares.”

The funds raised are put in to trust and are then able to be used only for an acquisition. The SPAC, having now gone public, trades like any other publicly traded company. Retail investors can purchase shares on the open market, even though the actual acquisition is not known (although the sponsor will generally give an indication of the market they are looking to target for an acquisition).

The position closer to home?

While the US market has boomed over recent months, the London market appears to be somewhat lagging. However, in a post-Brexit UK investment publicity drive, the UK Government has shown its eagerness to promote London as a SPAC investment centre with a review of the UK’s listing regime by Lord Hill specifically recommending changes in relation to SPACs to encourage their use.

Currently, trading in a SPAC’s shares is suspended once a target has been found in order to protect investors from price fluctuations. Lord Hill’s report recommends that this should no longer apply and that instead, stakeholders should be given increased rights to find out more about the proposed transaction, sanction the acquisition and redeem their shares. In addition, the report suggests the introduction of dual-class share ownership for a minimum of five years. This would potentially allow SPAC founders to retain a greater level of control for a certain period.

Given that the changes are unlikely to be introduced until much later this year, whether they are enough to increase SPAC activity in the UK will be interesting to see and may well depend largely on the media publicity surrounding SPACs.

The benefits of a SPAC?

The key benefit of a SPAC is that it is already public at the point of its acquisition. Provided that the sponsor finds a target company for it to acquire within the relevant time frame, the mechanism simplifies the process for a private company to go public with only an acquisition being required, rather than a listing.

From the point of view of the private company, not only is the process considered to be an easier way to go public, but it allows access to capital markets and the acquisition creates more certainty as to what funds will come in to the company and shareholders, as opposed to their being at the mercy and vagaries of the underwriters and market makers while trying to get the IPO away.

Shareholders in the SPAC are presented with the terms of the acquisition of the target company and then vote on the acquisition. If the shareholders don’t like the terms they have the power to vote against the acquisition, but if it proceeds they have the option to sell their shares while being able to keep their warrants, so can still benefit from an upside.

Some corporates are also looking at SPACs as a way to buy businesses they might not otherwise be able to afford from their own resources, i.e. by creating their own SPACs to look at possible acquisitions.

Advocates of SPACs claim that they make it easier for private companies to go public, with some describing them as “venture at scale” and some consider them to be an essential tool and option for private companies wanting to buck the trend of staying private for longer and raising money from alternative sources, such as sovereign wealth funds.

And the downside?

Critics of SPACs point to the fact that during 2020, SPACs gave poor returns on investments (although whether this is a trend or just short term will remain to be seen) and that sponsors are in it for their own ends without any regard or fairness for the public investors. According to figures by JP Morgan Chase, while sponsors have achieved an average return of 648% over the past two years, post-acquisition investors earned considerably less than that, with returns of just 44% (albeit some commentators may say that a 44% return in the current market given interest rates, for example, is still an attractive return). Others raise concerns that the business model incentivises doing something – anything – with other people’s money as opposed to making a true strategic assessment of opportunities, particularly if the clock is ticking before funds have to be returned.

Equally, the growth in the SPAC market could be its own challenge – with around 250 SPACs created over the past year, could this lead to parties chasing deals, overcrowding the market and overpaying for companies?

There is also a concern that some companies that would not be suitable for an IPO, or that would benefit from the rigour of an IPO process, could end up becoming public companies via the SPAC route when they would otherwise not persuade the market to take them on? (It will be interesting, for example, to see the fallout from the allegations surrounding one of the high-profile SPAC investments, Nikola Corporation, and whether that dampens SPAC enthusiasm).

Is increased “fairness” the answer?

Could the increased publicity surrounding SPACs and the competition element pave the way for some SPACs to offer “fairer” options for their public investors? A number seem to be taking this step, including:

Tying up sponsor shares for a certain period

Smaller sponsor stake

Correlating the sponsor stake with performance post-acquisition

It may be that in order for SPACs to continue to garner investor support and flourish as an investment tool, changes to their structure along these lines are inevitable and the market will, as it usually does, find its own balance in time.

Conclusion

Possibly the way to look at SPACs is the way one should look at most investment vehicles. None are perfect, some will suit certain types of investment and companies better than others and some will be more suited to professional investors rather than retail investors. On this basis, perhaps, for the right investment, there is space in the capital stack for SPACS to be a useful investment vehicle and option for some companies.

Lianne Baker is a Knowledge Development Lawyer in the Corporate team.

Disclaimer

This note reflects our opinion and views as of 17 March 2021 and is a general summary of the legal position in England and Wales. It does not constitute legal advice.

Our latest More Than Law podcast features our cross-departmental strategic land team, with host Miri Stickland talking to Partners Christopher Findley and Henry Cecil from the Rural Property team, Commercial Real Estate partner Ben Brayford and Planning partner Victoria Du Croz. Discussion points include what we mean by “strategic land“, who are the key parties and their particular drivers and concerns, and the key components needed for a successful strategic land development.

“Strategic land is basically land identified for the opportunity of new development, usually as a major extension of an existing urban settlement or a brand new residential-based development on a greenfield site. With it come the requirements for allocation in a local plan by the Local Authority, master planning to work out how much land you need to accommodate the number of residential units you are aiming to build, as well as the land assembly.”

“From the master developer point of view, they will be very invested in the success of the early phases of the development because the value of future plots will depend to some extent on how those early phases progress. You also need to consider the legacy and control aspects, which will be particularly pertinent to larger estates who will have a keen eye on the design and architecture of a development. Having discussions early on and understanding where the various parties’ pressure points are is going to be extremely important.”

Forfeiture Moratorium on UK Commercial Leases and restrictions on CRAR extended to 30 June 2021

11 March 2021

News

The government has announced that the measures which were put in place last year to assist commercial tenants during the Covid-19 pandemic will be extended, once again, to 30 June 2021.

The effect of the latest announcement is as follows:

Landlords will not be able to forfeit commercial leases on the basis of rent arrears until after 30 June 2021. Forfeiture for other breaches is still permitted.

Commercial Rent Arrears Recovery (CRAR) may only be exercised:

Between 25 March 2021 and 23 June 2021, if at least 457 days’ rent (i.e. five quarter’s rent) is outstanding when the notice is given and when the goods are taken control of for the first time.

On or after 23 June 2021, if at least 554 days rent (i.e. six quarter’s rent) is outstanding when the notice is given and when the goods are taken control of for the first time.

The government continues to encourage landlords and tenants to agree their own arrangements for paying or writing off debts, following the guidance set out in the Code of Practice governing commercial property relationships (“the Code”), which was introduced in June 2020. The Code seeks to promote open and constructive discussions between the parties where the tenant cannot afford to pay sums due. If arrangements are agreed, landlords should take care to ensure third parties like guarantors are not inadvertently released from liability.

Landlords remain able to pursue debt claims through the Courts in respect of unpaid rent and other sums. This is likely to remain the only option available to a landlord wishing to recover payment from tenants who can pay, but refuse to do so. A Judgment secures interest at 8% per annum on the sum due and can be enforced in various ways.

Landlords can still take action against guarantors.

There has been no comment on whether the restriction on using insolvency proceedings to recover sums due will be extended, but this seems highly likely to follow suit.

The government had previously said that the restrictions would end on 31 March 2021, and so the announcement is likely to come as a disappointment to many landlords. They do now appear to be looking to the future, however, and the press release gives some insight to the approach that may be taken when the restrictions are eventually lifted.

The government has confirmed that it intends to track the extent to which landlords and tenants are reaching their own arrangements under the Code. They indicate that they may take additional steps to protect business tenants if large numbers of landlords and tenants do not reach their own agreements, and there remains a significant risk to jobs. Both a phased withdrawal of current protections, and legislation to protect those businesses most at risk, are being considered.

Charlotte is a Senior Associate, and Ben and Jonathan are Partners in our Property Litigation team.